If you’re currently renting, one question we often hear is: “Can I afford to buy something instead?”. While every situation is unique, a helpful starting point is understanding how your current monthly rent compares to a potential mortgage payment.

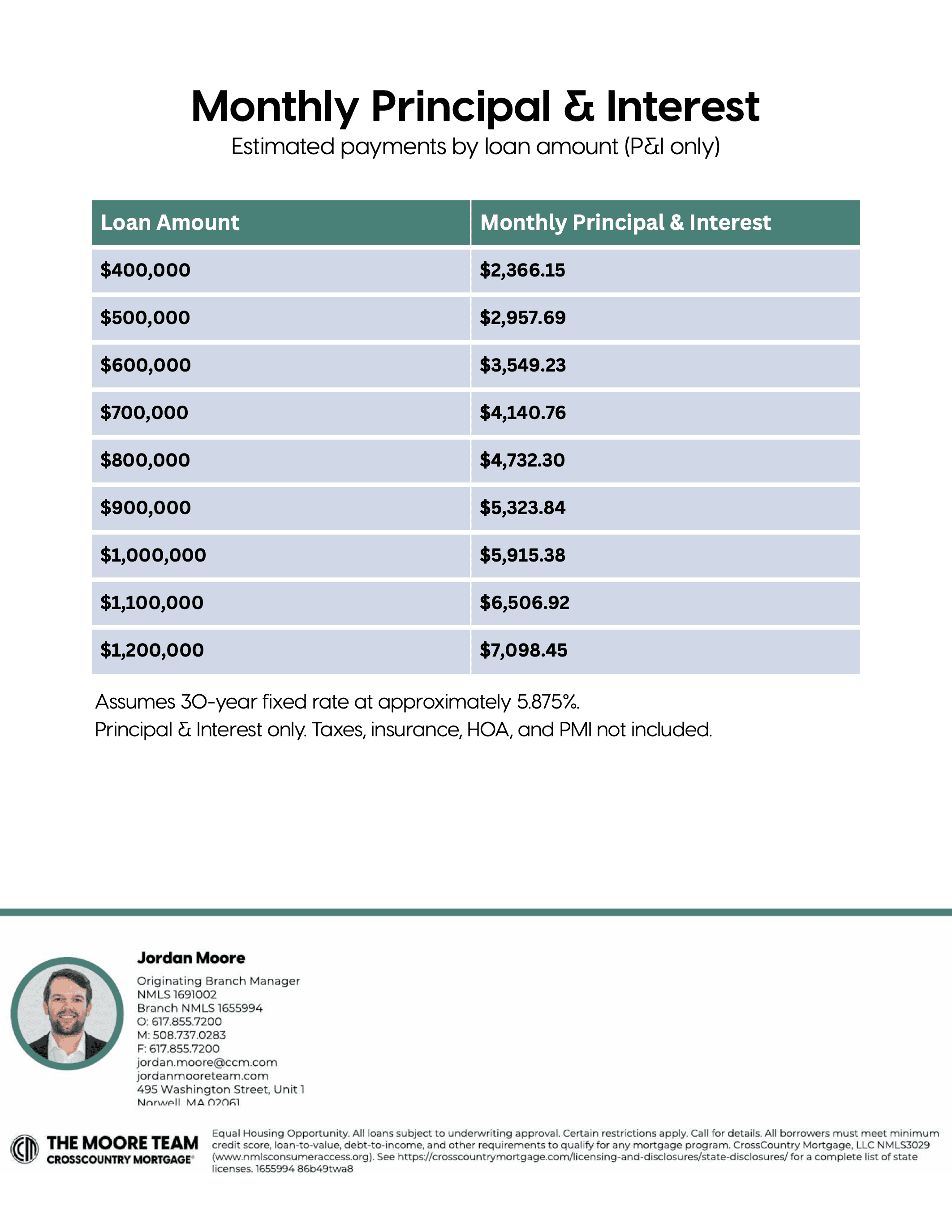

A recent chart shared by Jordan Moore of CrossCountry Mortgage provides a simple way to visualize this relationship – showing estimated monthly principal and interest payments across a range of loan amounts:

Important note: This chart does NOT include real estate taxes, condo fees or insurance, so there are some additional monthly expenses that need to be taken into account (see more on that below).

Buying vs. renting is something to consider because rent is a fixed cost with no long-term return; a mortgage payment, on the other hand, allows you to:

- Build equity over time

- Benefit from potential property appreciation

- Lock in a predictable housing cost (with a fixed-rate loan)

This isn’t to say buying is always the right move - but this chart helps highlight that the gap between renting and owning may be smaller than many people think.

What’s Right for You?

The goal isn’t to suggest that everyone renting should immediately buy. Instead, it’s to help answer a more informed question: “If I’m already paying $X in rent, what could that look like I owned?”

From there, we can evaluate:

- Your budget and comfort level, layering in other anticipated monthly costs, such as condo fees and real estate taxes

- Neighborhood and property options

- Long-term plans and investment goals

It’s a quick exercise and can help provide clarity on whether buying now, later or not at all makes the most sense for you. If you’re curious what your rent could translate to, reach out and we can run a customized analysis for you.